April 6, 2025

News

News

Liberation Day, uplifting economic data from the US, and cooling eurozone inflation

The US continued to show who’s boss, inflation in Europe continued to pick up, while the Chinese economy continued to slow down

.png)

The US continued to show who’s boss this week and I’m not just talking about Donald Trump’s expansionist rhetoric. Perversely enough, the strength of the US economy sent its stock market lower. Much more on that below.

🇺🇸 The S&P 500 fell 1.94% for the week after stronger-than-expected economic data raised concerns about inflation and higher rates in the US. The index closed yesterday at its lowest level since November 5 although it is still just 4.5% off of its record high set in early December. The Nasdaq Composite fell 2.34%.

The biggest story of the weak was undoubtedly the highly anticipated US non-farm payrolls report for December which came out on Friday. The number shows how many new jobs have been created outside of the agriculture sector.

The consensus forecast among economists was for 155,000 new jobs to be added. However, the number came in much higher than expected at 256,000. The number was even higher than the 212,000 jobs created in November which was also a big beat.

Furthermore, the unemployment rate ticked lower to 4.1%. Consensus was for the rate to remain unchanged at 4.2%.

Central banks around the world have been battling inflation in the past couple of years. They’ve been raising interest rates to slow down demand and the economy at large.

Prices, and therefore inflation, are largely determined by the supply-demand balance in the open market. Simply put, when consumers are employed, they’re able to spend. Thus, the stronger the job market and the lower the unemployment rate, the higher the demand for goods and services. Higher demand puts upward pressure on prices, aka inflation. At least in theory.

Higher inflation, or even just the fear thereof, will likely cause the US Federal Reserve to keep rates higher for longer. This is the part that had the biggest impact on the market.

Financial markets had an immediate and strong reaction to the jobs number. Here are some highlights.

In this upside-down perspective on the economy, the one “bright spot” in the report was that wages grew slightly less than expected at 3.9% year-over-year. This should at least dampen the Fed’s fear of inflation picking back up.

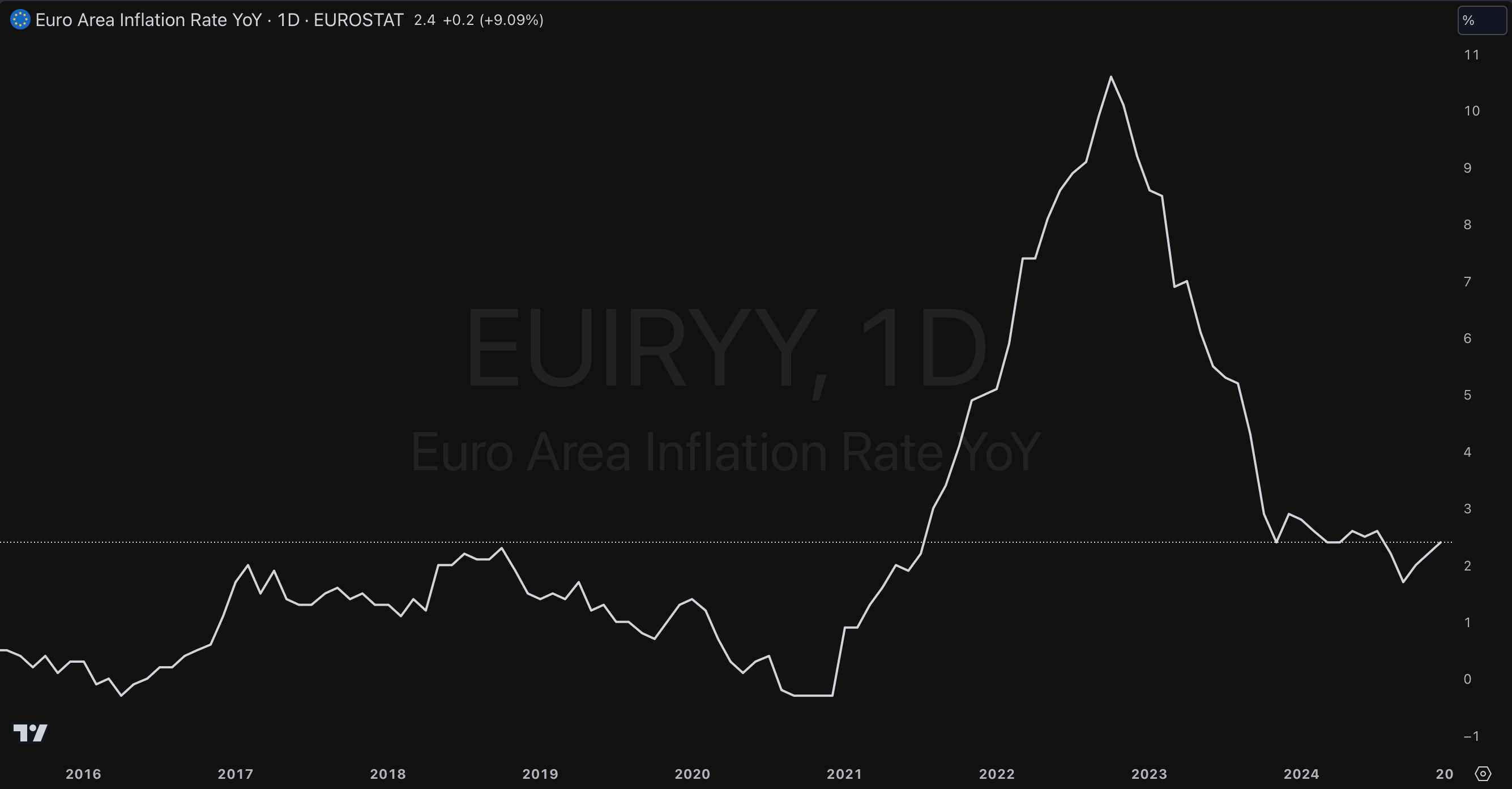

The latest inflation reading from the eurozone showed 2.4% year-over-year, in line with expectations. It increased for the third straight month, from its low point of 1.7% in September and 2.2% in November.

Core inflation, which strips out more volatile categories, landed at 2.7%. It’s been stuck between 2.7% and 2.9% since April last year.

Services inflation remains sticky as well, coming in at 4% where it’s basically been since November 2023.

Speaking of higher inflation, the latest update out of Germany did surprise to the upside. Inflation came in at a 2.8% annual rate in December, higher than the 2.6% expected. Prices rose 0.7% on a monthly basis.

Similar to the overall eurozone, inflation in Germany bottomed in September at 1.8% before rebounding to 2.4% in October and November.

So while the eurozone headline number is still close to the ECB’s 2% target, other measures are a little more concerning. If inflation continues to go higher, it also reduces the likelihood of more rate cuts to come.

That latter point also seemed to get reflected in the European bond market. The 2-year and 10-year yields both spiked more than 5.5% for the week, now sitting at 2.306% and 2.576% respectively. They have now rallied 22% and 27% since the bottom in early December. A big chunk of the gains this week came on Friday though, as bond yields seemingly jumped on the back of the US jobs report.

The stock market didn’t seem too worried about the higher rates though. The German DAX index rallied 1.56% on Monday and extended its gains on Tuesday. It finished the week 1.55% higher. The broad European STOXX 600 index gained 0.65%.

Another week, another economic blow for China. This time we got some important data points and a concerning move from the Chinese central bank.

First up, inflation. China’s consumer prices only rose 0.1% year over year in December, less than the 0.2% rise in November but in line with expectations.

Wholesale prices continued to do even worse, this time with a 2.3% decline year over year. It was slightly less bad than the 2.4% decline expected, but still not good. And it marked the 27th straight month of deflation.

Because while lower prices may sound nice, it spells big trouble for a growth economy like China’s. Stagnating or declining prices speak to slowing demand and poor growth.

One of the central bank’s recent initiatives to boost the economy has been massive bond buybacks with the aim of pumping some liquidity into the system.

These purchases have contributed to a big decline in bond yields which fell to new record lows last week. The 10-year yield dipped below 1.6% for the first time ever after dropping almost 20% in just four weeks, a very significant move for the bond market.

This has simultaneously weakened the Chinese yuan to a concerning level. The yuan currently trades at 7.362 against the dollar, a level it hit in October 2022 and September 2023. If it drops much further, below 7.375 to be exact, it will be the lowest level since 2007 where the Chinese economy (and the American for that matter) was in a completely different place.

A weaker yuan and lower bond yields make it less and less attractive for investors to keep capital in China, especially as yields in the US have gained additional traction in recent weeks.

The Chinese central bank confirmed what many analysts expected this week. It wants to defend the currency and do so immediately.

First step was to announce the issuance of a record 60 billion yuan ($8.2 billion) in central bank bills on January 15. Next up, the central bank stopped its bond purchases. These steps may have stopped the yuan’s freefall, for now, but China will likely have to do more than that to really shore up its currency.

The country appears to be stuck between a rock and a hard place though. Authorities want to increase liquidity to boost the slowing economy but they can’t do that without further devaluing the yuan. Something has to give. And that something may have to be the US dollar.

I’m very curious to see how Donald Trump will tackle the strengthening dollar when he takes office. It could definitely become a key part in negotiations with China. The US has the ability to weaken the dollar, thus strengthening the yuan in relative terms; But what does Trump want in return?

Elite level game of politics about to unfold. Get your popcorn ready.

Liberation Day, uplifting economic data from the US, and cooling eurozone inflation

Liberation Day tanks equities across the globe while crypto shows rare outperformance in risk-off environment

Trump slaps tariffs on autos while US inflation runs hot and consumer sentiment tanks