April 13, 2025

News

News

Trump rolls back his tariffs, US inflation cools, and big banks kick off earnings season with big beats

Happy New Year, everyone!

.png)

Happy New Year, everyone! We completed another year and kicked off 2025 this week. NYE also meant that most markets were closed for part of the week and we didn’t get a tonne of big news. However, there’s always something happening in the financial markets. Let’s take a look at the numbers and the main stories.

The US dollar index (DXY) topped 109.50 this week before pulling back to 108.92 on Friday. This marks another highpoint since the peak above 114 in the fall of 2022. And if we take out that brief period of time, the dollar hasn’t been this strong since 2002.

As with most assets, the price of a currency is defined by the supply and demand balance. Higher supply puts downward pressure on prices while increased demand pushes prices up. And there’s definitely been increased demand for the dollar lately due to the strong US economy and growth expectations, as well as higher rates.

The 10-year US government bond currently yields 4.60%. The 10-year EU bond yield, meanwhile, is only at 2.43%. A “risk-free” annual return of 4.6% makes US bonds a legit competitor to the equity market while the EU version will barely keep up with inflation.

Trade your euros, yen, yuan, or whatever currency you have for dollars and buy US government bonds. Higher demand for dollars drives up the price while doing the opposite to other currencies.

In oversimplified terms, a strong dollar is good for the local US economy and its consumers who benefit from cheaper imports and lower expenses when traveling. Non-US consumers and businesses experience the exact opposite.

On the other hand, a strong dollar hurts US companies that export to or operate in foreign countries. When they sell their goods or services in foreign currencies, they simply get fewer dollars in return when converting them to their base currency.

While I don’t think the current dollar level is anything to worry about, it’s worth following the development. It will eventually eat into US multi-nationals’ profits and hurt foreign businesses as well.

Furthermore, other countries may decide to intervene and strengthen their local currencies. The Bank of Japan did this in July, causing a big (but temporary) market crash.

It’s a complex topic and there’s a lot more to unpack. I will do a deeper dive into all of this in the near future.

China’s factory activity continued to grow in December, albeit at a slower pace than expected. The manufacturing index came in at 50.5, which still shows growth, but was significantly lower than the 51.7 measured in November and 51.5 expected for December.

Sales were dampened by falling export orders due to concerns about the trade outlook and increased tensions with the US after Donald Trump takes office.

Furthermore, China’s services activity jumped to a nine-month high in December, marking its longest growth streak since March 2023. Analysts point to the recent stimulus initiatives as a driver of increased local demand.

Speaking of which, the People’s Bank of China is reportedly preparing to cut interest rates even further in 2025 from the current 1.5% level. The country will also ramp up issuance of ultra-long bonds and efforts to boost local consumption.

None of this managed to bolster the stock market though. The mainland CSI 300 index plummeted 5.17% for its worst weekly performance in over two years. The Hang Seng held up significantly better but still declined 1.64% for the week.

China’s bond yields also continued their slump and hit new record lows this week. The 10-year yield declined to 1.598% while the 30-year dropped to 1.819%.

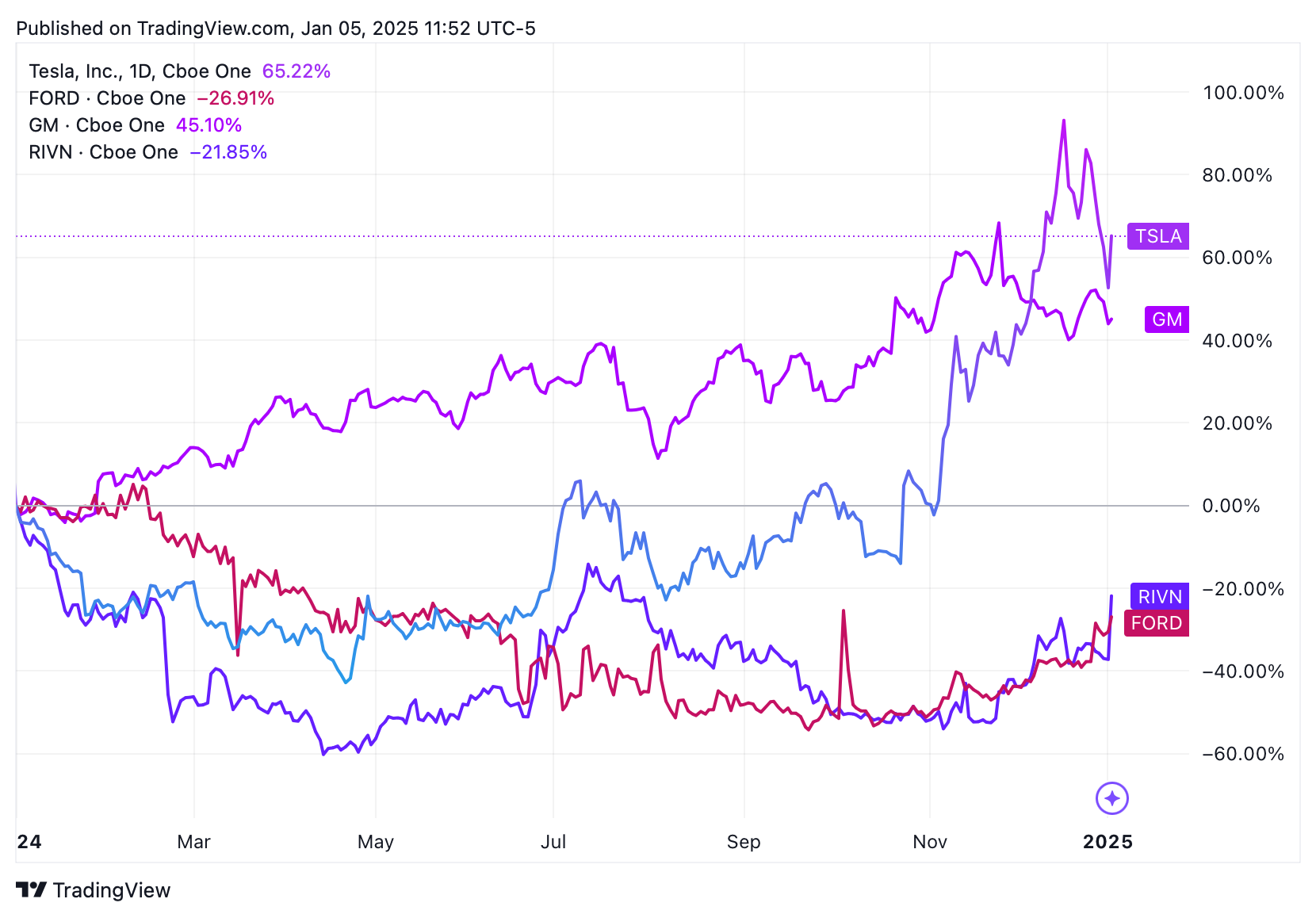

First up, let’s talk Tesla. Tesla’s Q4 delivery numbers missed the mark, coming in at 495,570 vs 504,770 expected. The company delivered a total of 1,789,226 vehicles in 2024.

What’s most notable about that number is that it was lower than the 1,81 million delivered in 2023. This marked Tesla’s first ever annual drop in deliveries.

The stock fell more than 6% on Thursday after the report.

On a much brighter note, however, Tesla reported on Friday that its China sales rose 8.8% to a new record in 2024. Shares all of Thursday’s losses and then some on Friday. It’s still down 16% from the peak on December 18 though.

Meanwhile, Ford and General Motors reported their best annual U.S. new vehicle sales since 2019. GM sold more than 2.7 million vehicles, 4.3% more than a year earlier.

Ford reported sales of 2.08 million vehicles, up from just under 2 million last year. The two companies have had wildly different years on the stock market, however. GM gained an impressive 48% in 2024 while Ford declined by almost 19%.

Last but not least, we got Rivian. Rivian had a rough 2024 where it lost more than 43% of its value. And that’s after being down as much as 63% at the bottom in April. Fast forward to Friday, Rivian stock had its best day ever with a 24.5% pop after reporting production and delivery numbers in line with expectations.

Trump rolls back his tariffs, US inflation cools, and big banks kick off earnings season with big beats

Tariffs kept dictating the market moves, both ups and downs, and resulted in a historically volatile week

Liberation Day, uplifting economic data from the US, and cooling eurozone inflation