March 29, 2025

Markets

Markets

The equity market at large took a big hit this week with US stocks reaching new local lows

PPI and CPI for December came in cooler than expected and sent risk assets higher while bond yields plummeted

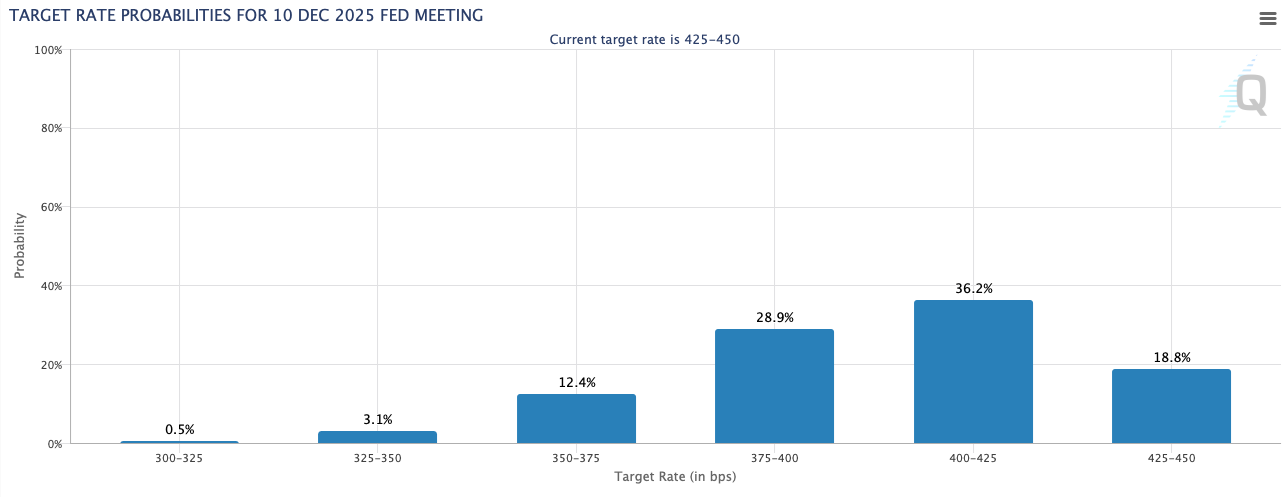

.png)

The main story this week was undoubtedly the latest round of inflation data from the US. After the Federal Reserve’s latest rate meeting, where they highlighted the risk of inflation picking back up, this week’s numbers were watched even more carefully than normal.

Investors want interest rates to come down but the Fed wants the inflation rate closer to its 2% target before cutting rates any further.

Thus, investors were praying for inflation data for December to come in lower than forecast this week.

On Tuesday we got the Producer Price Index (PPI). Here are the numbers:

Ad hen on Wednesday we got the Consumer Price Index (CPI):

Aside from the monthly headline CPI, the data was clearly positive. The most important of the data points, the core CPI, came in 0.1 percentage point lower than expected on both a monthly and annual basis. While that doesn't seem like a big deal, it was enough to boost investor confidence and alleviate fears of an inflation resurgence and rates staying higher for longer.

The market reaction on Tuesday was positive but muted. The 2-year yield declined 0.5% while the 10-year actually inched up. The S&P 500 eked out a gain of 0.11% while the Nasdaq declined 0.23%.

The reaction on Wednesday, on the other hand, was anything but muted. Maybe investors only care about the CPI right now or maybe they were just waiting for confirmation that the PPI data was actually reliable. Either way, the markets had a party on Wednesday.

Here are some highlights:

Stocks saw their best day since November 6 (election day) while Bitcoin once again topped $100k after hitting $89k just two days prior. Even the European STOXX 600 index came along for the ride, jumping 0.8% on the news.

Rate market traders now see a higher likelihood of two rate cuts than none in 2025, contrary to sentiment after Friday’s hot job report. Consensus is still for just one rate cut this year though, but the gap is closing.

One thing that stood out to me was the dollars' indecision. The dollar index (DXY) been rallying recently along with interest rates and did initially sell off on the cooler inflation data, as one could have expected. However, it quickly rebounded and now trades unchanged from pre-inflation data at 109.

After a few weeks of nervousness in the market, spurred on by hawkish and arguably aggressive rhetoric from the Fed and Donald Trump, a cooler-than-expected inflation print was exactly what the market needed to get back on track. At least for a while.

The Fed and investors alike are highly data-dependent at the moment. The next potentially market-moving data point will be the Personal Consumption Expenditure (PCE) price index, aka the Fed’s preferred inflation gauge. The December number will be released on January 31.

Before then though, the Fed’s next rate meeting is on January 29. Interest rates are almost guaranteed to be kept unchanged but Fed Chair Jerome Powell’s commentary will be closely analyzed.

Oh, and then there’s January 20 where Donald Trump will officially take office. He’s much better prepared than he was eight years ago and has already put a tonne of work in motion so I wouldn’t be surprised to see him make some big moves in his first few days. Could be geopolitical deals. Could be tariffs. Could be corporate tax cuts. Could be deregulation in certain sectors. It could even be about that strategic Bitcoin reserve he’s all but promised.

For now, it could seem like the market has at least a few days in the clear. The path of least resistance appears to be upward.

The equity market at large took a big hit this week with US stocks reaching new local lows

Trump slaps tariffs on autos while US inflation runs hot and consumer sentiment tanks

Interest rates steady in the US, UK, and Japan, a dovish Fed, and a massive spending package approved in Germany