April 18, 2025

Markets

Markets

US equities continued to struggle while most of the rest of the world continued its rebound

Macro data out of Asia and the US while equities managed to recover some of last week’s losses

.png)

It was a slow week in terms of news and markets around the world were closed for the holidays. We did get some interesting macro data out of both Asia and the US though, and equities managed to recover some of last week’s losses.

Japan’s industrial output declined for the first time in three months, falling 2.3% in November. That’s down from a 2.8% increase in October but still much better than the -3.4% expected.

Industrial product also declined on an annual basis, shrinking 2.8% from a year ago.

Retail sales data surprised to the upside as well, growing 2.8% year-over-year in November vs 1.6% expected. It was also significant acceleration from 1.3% in October.

On a monthly basis, retail sales grew 1.8% in November for its fastest rate since September 2021. This was the first increase in three months.

In other news, the latest reading of Japan’s unemployment rate showed 2.5%, matching market expectations and remaining unchanged from the month prior.

Perhaps a little too upbeat was the latest inflation reading from Tokyo. The consumer price index (CPI) jumped 3% year-over-year in December, its highest level of the year.

The hotter inflation increases the likelihood of more rate hikes from the Bank of Japan who made its first hike in 17 years when it brought rates from negative 0.1% to 0.1% in March this year. It hiked again in July, taking rates to 0.25%.

And on the note of rate hikes, a summary of the BoJ’s latest meeting showed that it is indeed ‘likely to hike in the near future’.

All in all, the market seemed to like the data. The Japanese Nikkei 225 index rose more than 4% for the week and closed at its highest level since July. It’s now up more than 20% for the year.

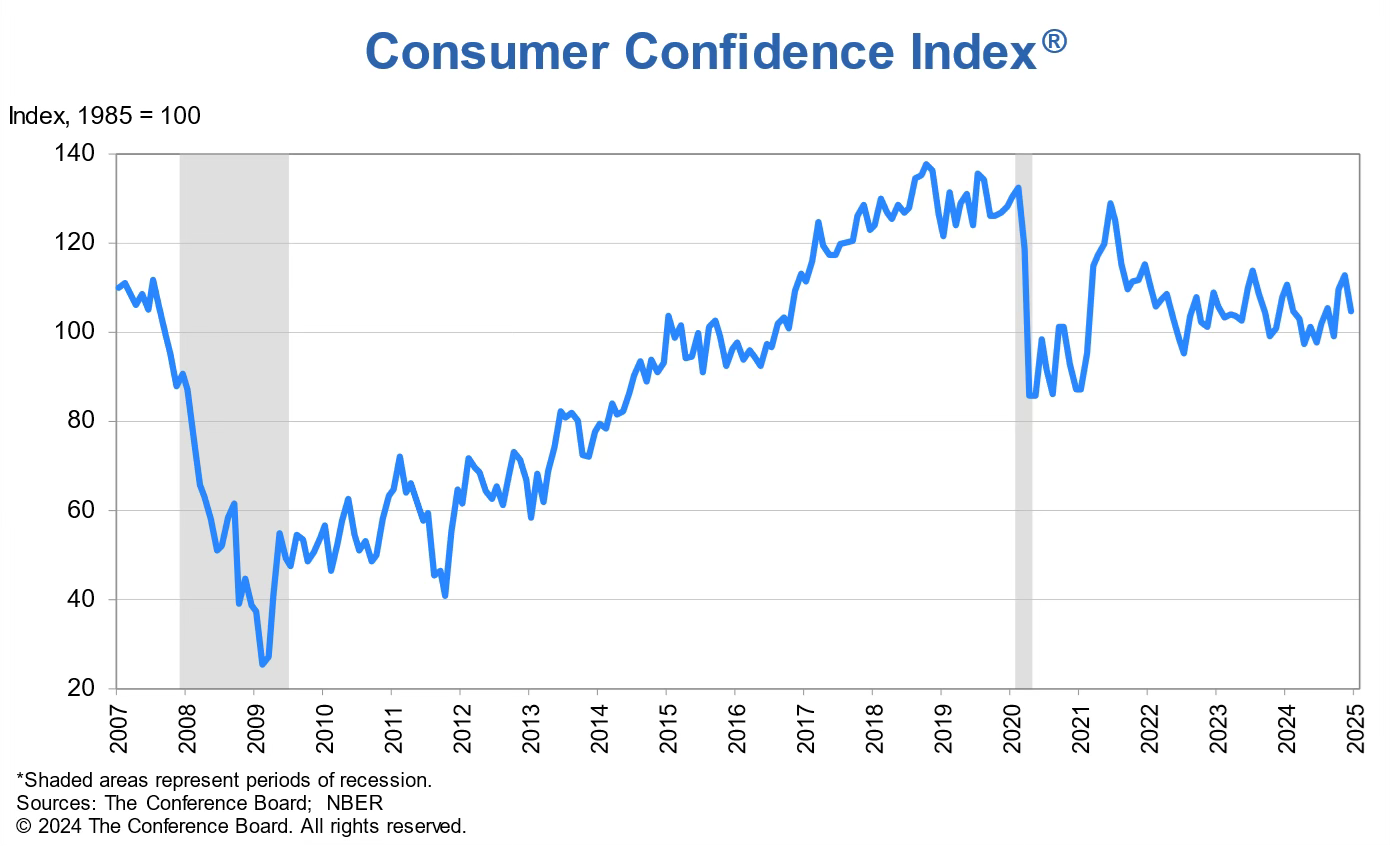

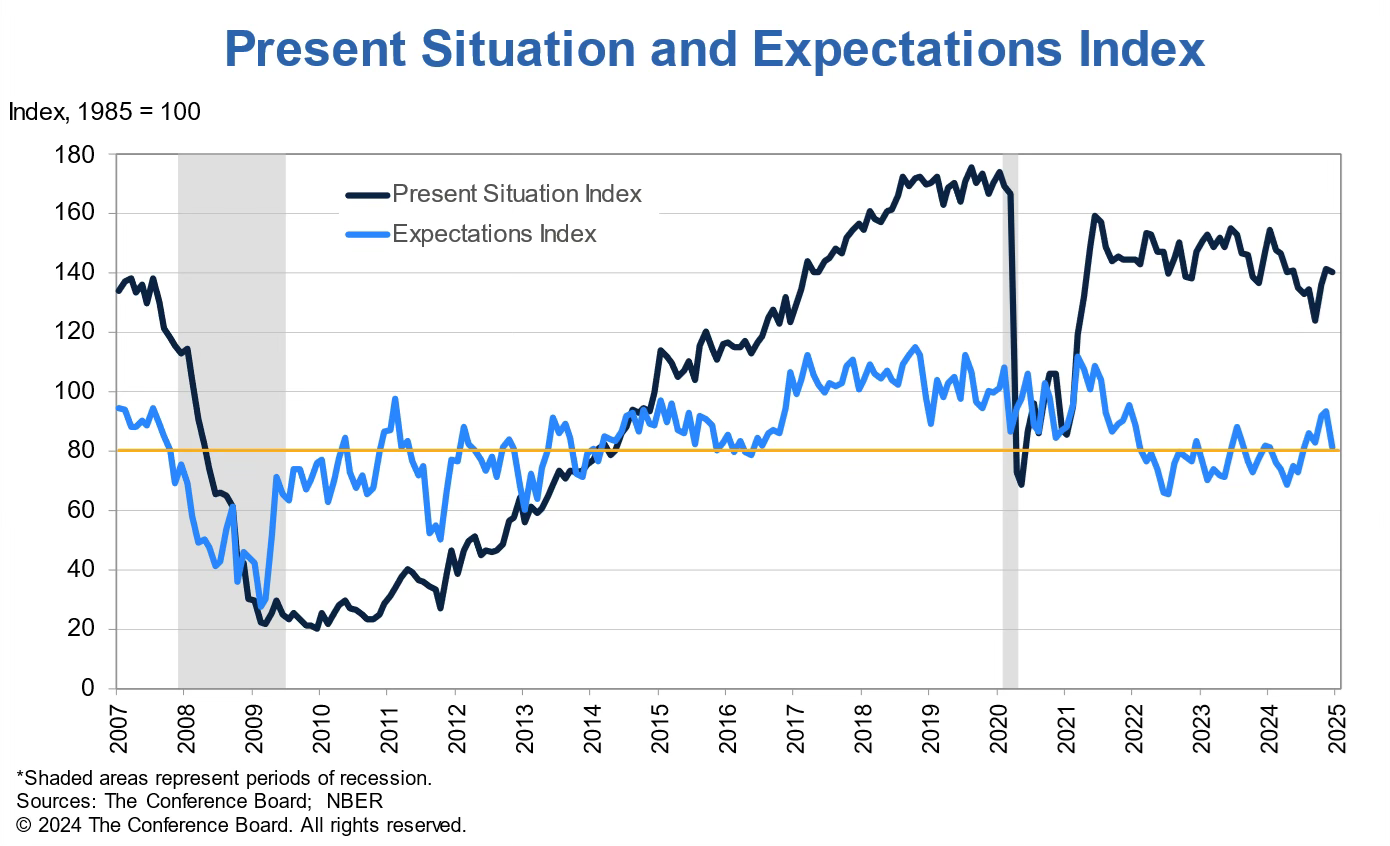

The Conference Board’s consumer confidence index came in at 104.7 in December. This was down by 8 points from 111.7 in November and well below the 113.2 expected by economists surveyed by Bloomberg.

Zooming out, however, the data point doesn’t look bad at all. The index was hovering around 100 for most of 2024 until it took a jump up to 109.6 in October.

The expectations index, which includes the short-term outlook for income, business, and labor conditions, told a similar tale, dropping 12.6 points from 93.7 in November to 81.1 in December.

Some analysts are concerned about this because of the notion that the 80 level has historically signaled a recession ahead. However, that hasn’t really been the case since the great financial crisis in 2008 - 2009.

In fact, the expectations index was below 80 for the better part of four years after the recession ended in 2009. And more recently, the index only had brief spikes above 80 from the start of 2022 to the latter half of 2024. While a recession may come in 2025, the index clearly hasn’t worked as an accurate predictor.

Furthermore, the Federal Reserve may actually welcome a slowdown in consumer sentiment to combat inflation. This may be what we need to finally close that chapter and enable the Fed to make some significant rate cuts next year. If this latest sentiment data is in fact accurate, that is.

These indices are interesting to follow because of how much attention they get, but it’s important to separate signal from noise. As with most charts, nothing goes up (or down) in a straight line. The December data point looks like noise in the trend that’s been in place for almost three years: Consumers feel fine, both about the present and the near future.

China plans to issue a record $411 billion (3 trillion yuan) worth of special treasury bonds next year, three times as much as this year.

What’s really interesting about this is that the proceeds will be used to boost consumption via subsidy programmes, equipment upgrades by businesses, and funding investments in innovation-driven advanced sectors.

The move underscores China’s commitment to support its local economy and soften the blow from a potential trade war with the US.

China’s 10-year and 30-year treasury yields rose 1 and 2 basispoints respectively on the news, although the latter gave it all back with a 3% drop on Friday. The Hang Seng index rose 1.87% during the holiday-shortened week.

US equities continued to struggle while most of the rest of the world continued its rebound

Trump rolls back his tariffs, US inflation cools, and big banks kick off earnings season with big beats

Tariffs kept dictating the market moves, both ups and downs, and resulted in a historically volatile week