April 18, 2025

Markets

Markets

US equities continued to struggle while most of the rest of the world continued its rebound

We got inflation data from the US and a series of macro numbers from China while Trump remained in the headlines

.png)

Most financial markets took a bit of a breather this week after last week’s red-hot Trump rally. We got inflation data from the US and a series of macro numbers from China. Trump remained in the headlines as well. Before diving into that though, here’s a quick market recap.

Thanks for reading Money by CJ! Subscribe for free to receive new posts and support my work.

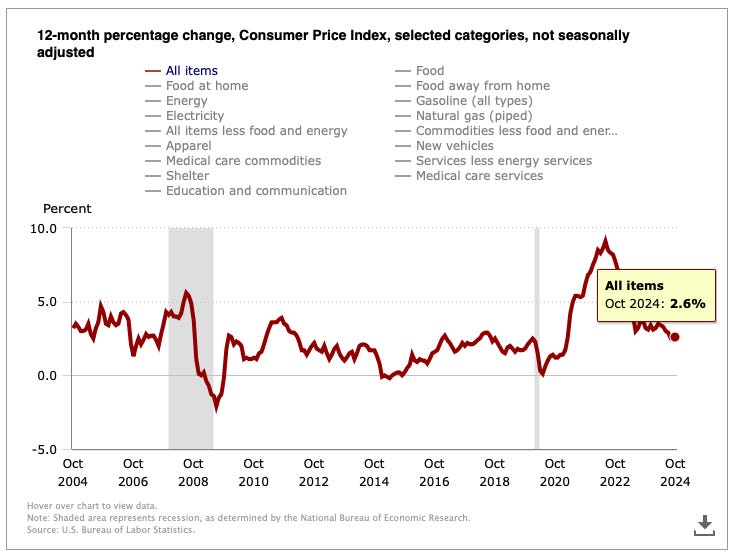

The Consumer Price Index (CPI) rose 0.2% in October and 2.6% for the year in the most recent report. Both numbers were in line with expectations.

Core inflation, the data that excludes more volatile categories like food and energy, rose 0.3% for the month and 3.3% for the year.

The Producer Price Index (PPI) came in at 0.2% for the month and 2.4% for the year, both in line with expectations. Core PPI was at 0.3% for October and 3.1% for the year, also as expected.

Services rose 0.3% for the month and accounted for most of the increase in PPI. And most of this was attributed to Portfolio Management prices which jumped 3.6%.

Both food and energy prices actually fell on the month, 0.2% and 0.3% respectively.

While the numbers ticked up slightly from last month, they still show that inflation has been tamed and is very close to the 2% target. Especially when compared to the peak in the summer of 2022.

The market currently sees a 62% likelihood of a rate cut at the Fed’s next meeting in December. The number was 82% on Wednesday, a day before the PPI data was released.

The Fed raised rates aggressively to combat inflation but has started lowering them in response to cooler inflation. A pickup in inflation will likely push the Fed to keep rates higher for longer.

What’s interesting is that Donald Trump campaigned heavily on inflation still being a major issue. And one that he can fix. Voters seemed to agree with both.

However, some of Trump’s planned policies are seen as rather inflationary. Take tariffs on imports and massive tax cuts, for instance. One literally makes products more expensive while the other boosts consumer spending which is likely to fuel price increases.

It will be interesting to see which of his suggested initiatives are actually implemented and to what extent. And then we’ll see the impact on inflation.

We got a big bag of macro data out of China on Thursday. All in all, I think it’s fair to say that the data was mixed, at best.

On the positive side, retail sales in China grew 4.8% year over year, well above the forecasted 3.8%. It was also significantly higher than the 3.2% annual growth reported in September.

However, industrial production growth fell short of expectations, coming in at 5.3% vs 5.6% expected.

Furthermore, investment in real estate fell by 10.3% for the January to October period. That’s worse than the 10.1% decline seen from January to September and the biggest drop since the year-to-date period ending in August 2021.

So far this year, the value of new properties sold is down 20.9%. While that sounds pretty horrendous on the surface, it was actually better than the 22.7% drop reported as of September.

Unemployment in cities fell from 5.1% to 5%. We’re still awaiting an updated figure for youth unemployment which fell from a record high 18.8% in August to 17.6% in September.

What we’re also awaiting is for the recent stimulus measures in China to take hold and make a real impact on the economy. For now, many investors remain skeptical of their efficacy.

And then there’s the whole tariff situation. How aggressive will Donald Trump be when he formally takes office in January and how big of an impact will he have on the Chinese economy?

There’s a lot of “wait and see” going on in China at the moment and the consensus approach among investors seems to be one of caution.

Donald Trump was busy assembling his new team this week, appointing several people for key roles in his upcoming administration. Here are a few highlights and their potential impact on the financial markets.

Donald Trump picked Marco Rubio for Secretary of State. He’s known for a very hawkish stance on China so we should probably expect the trade war to ramp up. Think higher tariffs and potential import bans of China good to the US.

In addition to being a risk for Chinese companies and thus the stock market, slapping tariffs on imported products is also inflationary. An increase in inflation could both hurt the US consumer and force the Fed to keep rates at a higher level than many investors hoped and expected.

Next up, Trump tapped Robert F. Kennedy Jr. for Secretary of the Health & Human Services Department. As a known vaccine skeptic, the pick unsurprisingly sent vaccine stocks lower on Thursday and Friday. Moderna and Pfizer, two Covid-19 high-flyers, dropped 7.34% and 4.69% respectively on massive volume. The stocks were already struggling though.

RFK is also highly critical of our health and food system overall. He sees some fundamental problems in the prevalence of processed food, pesticides, prescription drugs, etc. in modern society.

If he gets approved for the role and is able to follow through on some of the things he really cares about, the impact could be massive for a variety of industries and individual companies.

Will he make lives tougher for fastfood restaurants and processed food manufacturers? And help restaurants and companies focused on healthy food? Will Eli Lilly and Novo Nordisk be able to sell as much of their weight loss drugs if people actually begin eating healthier? Will he outright ban pharma companies from running ads on TV (an idea he’s floated before)?

There’s a series of potential impacts to consider if someone as radical as RFK gets appointed to the role of Health & Human Services secretary. It’s not official yet though, so I’ll be paying close attention to the story and do a deep dive at a later point.

Last but certainly not least, Trump appointed Elon Musk and Vivek Ramaswamy to lead the newly formed Department of Government Efficiency (DOGE). It’s unclear to me what impact this will have on the financial markets, except for one: The recently created D.O.G.E. meme coin, obviously.

The D.O.G.E. token was created in August when Elon Musk first started talking about the new department and peaked above a $500 million market cap on the heels of the official appointment this week.

So, to conclude: Elon Musk and memes keep winning. We live in interesting times.

US equities continued to struggle while most of the rest of the world continued its rebound

Trump rolls back his tariffs, US inflation cools, and big banks kick off earnings season with big beats

Tariffs kept dictating the market moves, both ups and downs, and resulted in a historically volatile week